The Institute for Security and Technology’s Strategic Balancing Initiative (SBI) is currently engaged in working group meetings with technologists and industry leaders across different domains. Through these meetings, SBI aims to brainstorm creative policy solutions to increase American innovation while addressing the national security concerns prevalent in the larger context of U.S.-China techno-industrial innovation. Currently, many of our discussions focus on “commons” or “sandbox” infrastructure solutions that offset misalignments in cost, risk, and timelines.

The semiconductor industry is the easiest case study to examine, as the newer CHIPS and Science Act (CHIPS Act) incentives are currently in the spotlight, including manufacturing and tax incentives, workforce incentives, and ecosystem support such as through the creation of the Department of Defense’s Microelectronics Commons and the Department of Commerce’s National Semiconductor Technology Center (NSTC). Previous analysis of the CHIPS Act highlights how such incentives impact Integrated Device Manufacturers and their supply chains. Additionally, other analysis shows that the $52.7 billion provided by the CHIPS Act is not, by itself, sufficient to reshore supply chains. However, SBI’s working group meetings have begun to explore the significance of the other side of the industry: startups. An examination of the value of semiconductor startups illuminates the need for ecosystem support across all aspects of the chip development value chain, the interplay between “promote” and “protect” policies (i.e. incentives and export controls), and, ultimately, suggests that American policy needs to not only sustain but amplify innovation in the short-term.

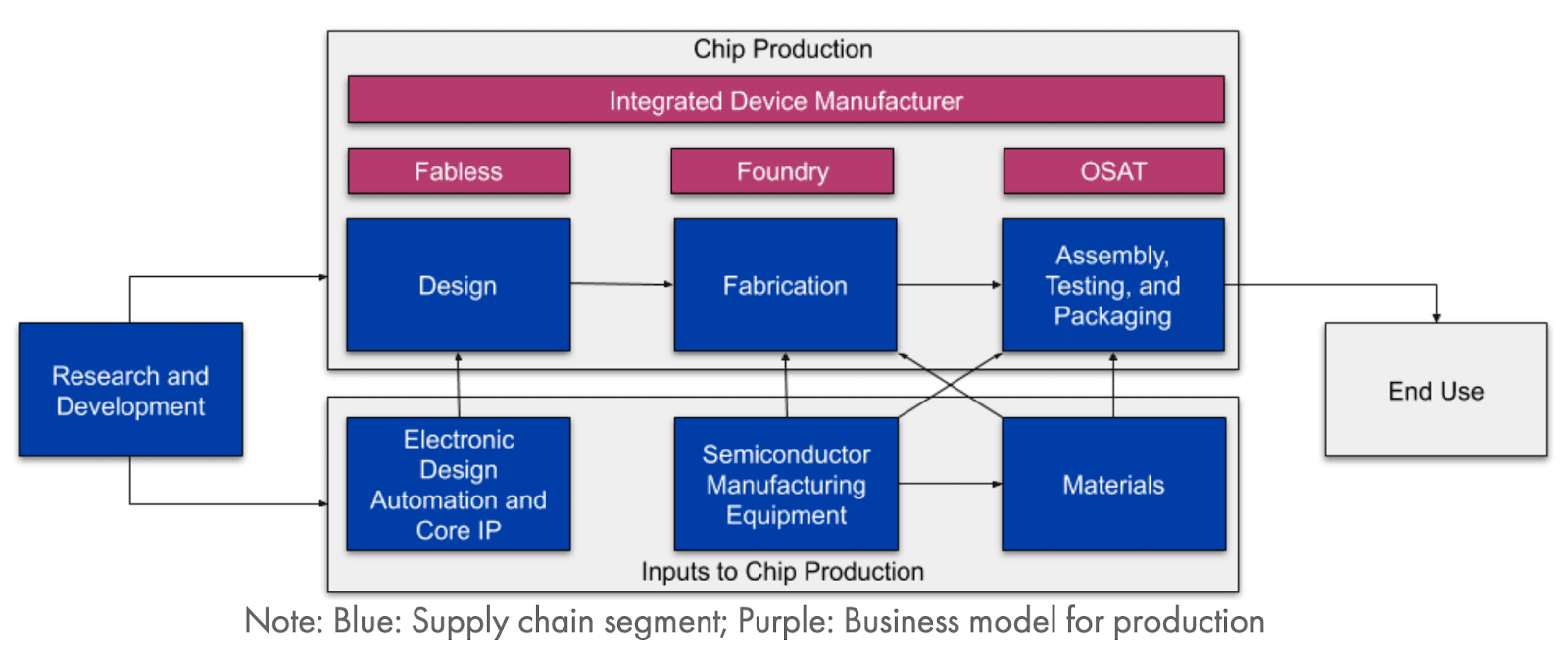

Saif M. Khan, Alexander Mann, Dahlia Peterson, “The Semiconductor Supply Chain: Assessing National Competitiveness,” Center for Security and Emerging Technology, https://cset.georgetown.edu/publication/the-semiconductor-supply-chain/

SBI’s focus on startups is not inherently profound. Consider diagrams such as the one above depicting the semiconductor development value chain and imagine tiny arrows surrounding each aspect – design, fabrication, packaging, etc. – to represent startups’ contributions. Put simply, startups may innovate on one small segment of the semiconductor value chain. This could entail innovating on a niche application of a technology, such as integrated circuits in an extreme environment, or even crossing into multi-sector solutions such as AI or materials. Due to their very nature as small, new entities with little funding, startups encounter barriers such as high costs for lab space, costs associated with downstream or upstream technology or processes, high costs for manufacturing or prototyping at a smaller scale, and a lag in return on investment. Some of these barriers we see acknowledged in recent CHIPS Act initiatives. For example, A Vision and Strategy for the National Semiconductor Technology Center mentions startups and the need for fabs to support shuttle runs at rates at or below market in recognition of the associated cost and scale barriers. The NSTC also includes the creation of an investment fund to bolster startups as well as spur collaboration between existing entities to help commercialization. And this is not to ignore other small business initiatives in the ecosystem, such as the National Science Foundation’s Small Business Innovation Research (SBIR) / Small Business Technology Transfer (STTR) funding.

The Interplay Between Protect and Promote

Things get interesting when we take these considerations and shift to the “protect” side of U.S. semiconductor policy. Recent analysis highlights how the United States’ export controls will incentivize China’s development of its own indigenous capabilities. In other words, export controls are time-bound: stopping technology transfer completely isn’t possible; in the long-term, choke points will no longer be choke points. Similar and related to the restriction of Graphical Processing Units and other AI-enabling technologies, restricting exports seems to function in conjunction with the domestic push to arrive at the next technology breakthrough faster – to become a first mover of a capability or technology in all aspects, from capturing market share to integrating with national security efforts.

Finding the American System’s Differentiator

Restricting and failing to innovate while China is developing its own capabilities will not lead to a technology advantage. And China is certainly developing. Rather than reciting China’s high-level policy documents, I want to instead turn to its National Integrated Circuit Industry Investment Fund (国家集成电路产业投资基金股份) despite its suspension in 2022. The fund was initially endowed with around $23 billion with $21 billion raised in its second phase, and has since led to the creation of sister funds at local levels and significant mergers and acquisitions. Notably, the fund has subsidized domestic competitors to historically U.S.-dominated chips. Ultimately, the fund is a perfect example of how significant incentives are created by Beijing (even with some pauses). In contrast, not only does the United States not fund national champions and create state-backed subsidies in a way equal to China, but private investment also tends to prioritize other industries over semiconductors.

The United States is not China, nor should it try to be. I am not suggesting that the United States needs its own National Integrated Circuit Industry Investment Fund. There are mechanisms that work within China’s market and governance structure that simply would not work in the United States. This is where we turn to American advantages and concepts like open research and attracting and retaining talent that are crucial drivers of innovation.

Social, Educational Factors Amplify Technology Incentives

If the deciding factor in U.S.-China techno-industrial competition is the ability of American industry and government to innovate faster than their Chinese counterparts in the near-term, then initiatives like those born from the CHIPS Act need to be not only self-sustaining, but also amplifying. At a high level, industry partnerships between manufacturers, national labs, universities, startups, and companies that address issues such as the lab to fab gap need to not only persist but deepen. Additionally, such efforts need to be integrated with other ecosystem-supporting policies that not only address technology, but also educational and social aspects as well–many of which are in fact ingrained in the CHIPS Act. The alignment I am calling for is also partly an alignment between international, domestic, federal, and state-level policy. It’s hard to have technology startups if there’s a lack of STEM education and workforce development. It’s also hard to attract talent if the talent isn’t incentivized to make the United States their home – a point emphasized during one of our off-the-record conversations with an academic involved in university-grown startups.

Through SBI’s examination of both the role of startups as well as their barriers to success in the semiconductor industry, it is clear that the success of national-level policy will be impacted by not only its implementation, but also the integration of that policy with supportive national and local-level initiatives. The layers of community, city, state, and national policy that we are seeing develop in this sector reveal the wide breadth of stakeholders involved as well as the deep levels of integration with other niche technology ecosystems. As Commerce, Department of Defense, and other government stakeholders continue to develop CHIPS Act-created initiatives, it will be vital that they work to make these initiatives sustainable and amplifying.

As our work in the Strategic Balancing Initiative continues to accelerate, we will explore how venture capital, startups, and other technology stakeholders contribute to U.S.-China techno-industrial competition. Stay tuned for future updates on policy recommendations, analysis across different technology sectors, and outputs from future working groups.